Article | Basics 6: "How Do the Watchmen Watch?" - State Compliance Monitoring Procedures

Apr 06, 2022

Inspection Basics

Recent Update!

Recent Update!

- The new regulations no longer require that the state HFA examine the same units when conducting file reviews and physical inspections. In fact, they prohibit doing so, unless the inspections are conducted on the same day. This keeps the units unannounced for each part of the review.

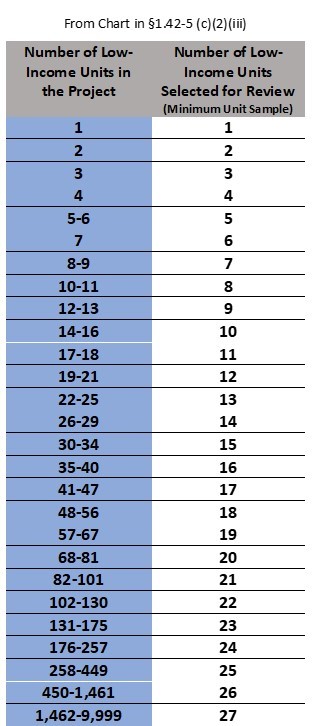

- If units that are selected do not cover all buildings, the HFA must select some aspect to inspect buildings that will not have any units inspected. These can be building exterior, HVAC, or similar.

- The reasonable notice time that states are allowed to give of an upcoming inspection has been reduced from 30 days to 15.

- An exception exists for LIHTC/HUD properties that are monitored by HUD REAC inspections, which may use the REAC sampling methods and this means that often all buildings are not inspected.

- The HFA may not inform the owner which units will be inspected prior to the day of the inspection

Bonus | COVID 2022 Adjustments

During the COVID era, the IRS issued a series of Notices that waived some of the inspection rules. IRS Notice 2022-5 adjusted some provisions that affect the Treas. Reg 1.42-5 inspection rules through 2022. Correction periods were adjusted as well as an allowance for states to suspend physical inspections through 2022 if the HFA determines it is needed. All of the provisions of the Notice can be a bit complicated, so we have designed a chart to help. Download the chart HERE.

Helpful Hints

-

Arrive on time for the audit.

-

Have a place prepared for the reviewer to review files. Adequate light and a surface to work on are important. Even a folding table in a laundry room is better than nothing at a property without office or community room space.

-

Have all files on hand.

-

Find out if the auditor prefers the manager to stay close at hand to answer questions or would rather they wait to answer all their questions at once. This is a matter of individual auditor taste.

-

Notify all residents of the physical inspection, giving sufficient time under the property lease and state law. Also, have keys on hand for all units. If the inspector cannot legally enter units, the state HFA is very likely to declare all of the inaccessible units noncompliant.

-

Do not be defensive or argumentative. Make sure that all interaction with the reviewer is professional. If the auditor is wrong on a point, a chance to dispute the matter will come when the written report is received later. Many incorrect findings also disappear once an auditor has a chance to do some research of their own. Getting into a conflict does not serve anyone’s interests.

-

Respond quickly to health and safety issues and inform the HFA immediately when these are addressed. The inspector will provide the timeframe for corrections, generally 24-72 hours.

-

The HFA may send the report to the owner or a key person at the property management company that may not be the site manager. The site manager should make sure that they ask this person if the letter has arrived regularly until it comes. This prevents unnecessary delays in getting started on the fixes.

-

If the auditor conducts an exit interview, begin corrections as soon as possible. If not, work should begin as soon as the letter is received. The state is required to give a limited time for corrections to be made before a form 8823 must be submitted to the IRS.

Correction Periods

The state HFA is required to inform the owner of the findings of the audit promptly. From the time of notification, the HFA will provide a correction period. This can be up to 90 days as the state dictates. If an owner/agent can make a case for unusual extenuating circumstances, the state may allow a total correction period not to exceed 6 months. It is in the property's best interest to make all corrections possible in the state-dictated correction period. This way the noncompliance will be reported to the IRS as "corrected" and may receive less scrutiny from the IRS and decrease the chance of a full audit.

Due Diligence and File Audits

“Compliant behavior can be demonstrated when a LIHC property owner exercises ordinary business care and prudence in fulfilling its obligations. Due diligence can be demonstrated in many ways, including (but not limited to) establishing strong internal controls (policies and procedures) to identify, measure, and safeguard business operations and avoid material misstatements of LIHC property compliance or financial information.”

-

Separation of duties,

-

Adequate supervision of employees,

-

Management oversight and review (internal audits),

-

Third-party verifications of tenant income,

-

Independent audits, and

-

Timely recordkeeping.”

The above topic is just one of many to be discussed at this year's Compliance Summit Events. Check it out HERE!

The above topic is just one of many to be discussed at this year's Compliance Summit Events. Check it out HERE!

There is a very good chance that the topic of this post is covered in an online on-demand course at Costello University.

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.