Article | Basics 9: "When Old is New Again..." Acquisition/Rehab Overview

Jul 06, 2022

In this series, we have covered the basics of tax credit compliance and how to research answers to questions tax credit professionals have in their daily practice. In this Basics article, the focus will be on compliance for acquisition/rehab (acq/rehab) properties.

All tax credit properties are fairly complex. They can be likened to a machine with many moving parts to run smoothly. Existing buildings that are acquired and rehabbed with tax credits involve additional “parts”, including communicating with the existing population, construction around them, and unit transfers. From a compliance standpoint, there are also several complex issues to be aware of and incorporate into all the other “moving parts” of successful tax credit delivery. It becomes clear to seasoned professionals that there are several key differences in carrying out compliance for new construction as compared to acq/rehab properties. Understanding where these project types differ helps housing professionals avoid the confusion that sometimes can accompany acq/rehab compliance. In this article, several of these differences will be highlighted.

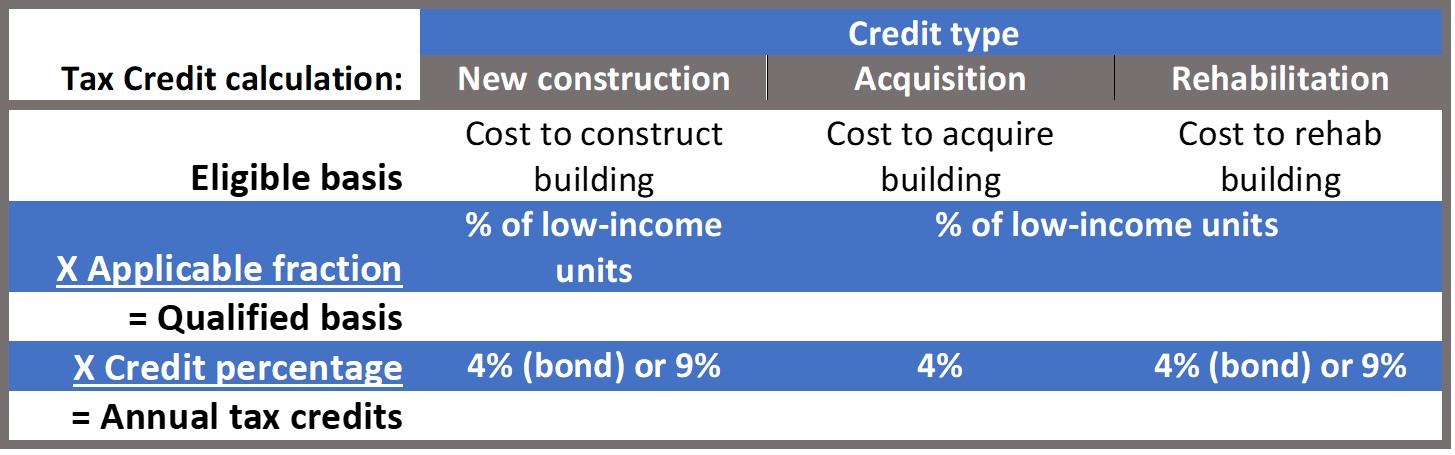

Two Credit Streams

The value of tax credits has as a starting point depreciable costs spent on a housing building. The accounting term for these costs is the eligible basis for a building. New construction costs are a common basis for tax credits. In addition, the costs to rehabilitate an existing building may be a basis for credits. Finally, the cost of acquiring an existing building can be used, as long as the building will also be rehabbed. As the costs that go into the eligible basis for the acquisition of an existing building are different from the costs for rehab of the building, each basis establishes a separate credit stream. As each of these credit streams must be accounted for separately, each building subject to acq/rehab will have two allocation forms 8609.

Applicable credit percentages may also differ between the credit streams. The rehab credits can have a 9% applicable credit percentage as long as the rehab is not financed with tax-exempt bonds. Acquisition credits, however, are always limited to a 4% credit, regardless of financing.

Placing In-Service and the Start of Credits

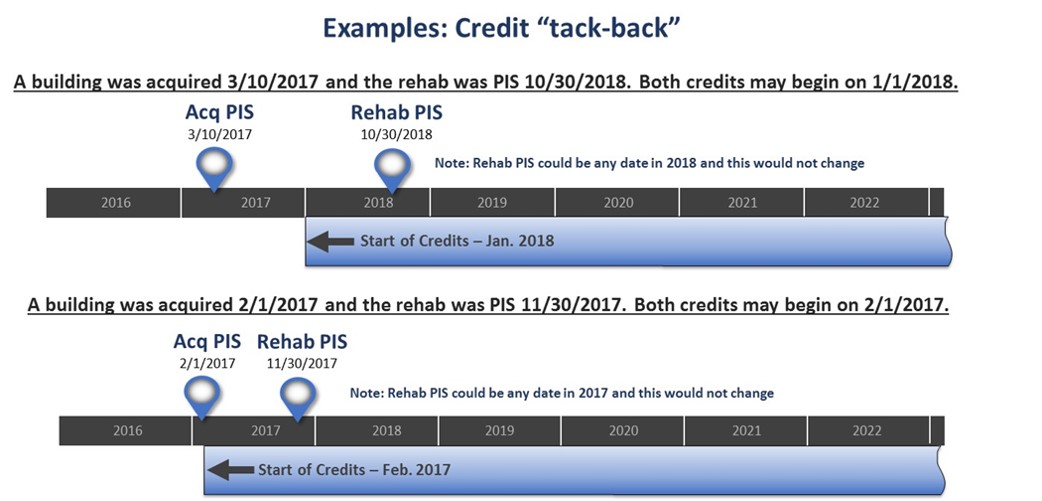

A sometimes-confusing crucial difference between acq/rehab projects and new construction is how placed in-service dates and the start of credits work. Per IRS guidance, a tax credit building is placed in service when it is ready for its intended purpose. For new construction, this is generally when a certificate of occupancy allows an owner to legally occupy the first unit in a building, with occupancy being the intended use of the building. This date becomes important as a starting point. Leases and resident occupancy should not predate the placed in-service date for a new construction building. Also, tax credits cannot be claimed on a building until on or after its placed in-service date. For existing buildings that are occupied at acquisition, however, the building is ready for its intended occupancy purpose as of the acquisition, thus the placed in-service date is the date of acquisition. The definition of placed in service for rehab is based on an expenditure test (how much is spent) that involves time limits and minimum expenditures to establish the needed eligible basis for the rehab. The date is not necessarily directly related to when the rehab is completed or when all units are suitable for occupancy. Because of this, each acq/rehab building has two placed in service dates, one for the acquisition and one for the rehab. Each date will show up on its respective 8609.

As with new construction, acq/rehab credits cannot be claimed until a building is placed in service. In theory, this means that both credits could start as early as the acquisition is placed in service. However, if the rehab is placed in service in a later year, then both credits will start as of the start of the year that the rehab places in service. Note that this is not the rehab placed in service DATE, but rather it is the YEAR the rehab is placed in service. Thus, is can be said that credits may start the later of the acquisition date or the start of the year the rehab is placed in service. If a building is acquired on February 1, 2018, and the rehab is placed in service (enough money is spent) by November 17, 2018, both credits may be claimed starting February 1, 2018. Alternatively, if the rehab was not placed in service until March 13, 2019, both credits may begin the start of 2019.

With new construction, once a building is placed in service, credit may either be claimed starting that year, or they may be deferred one year. This is also true for an acq/rehab project. However, the deferral option is based on the year the rehab is placed in service, not acquisition. In the above scenario where the building was acquired in 2018, but the rehab was placed in service in 2019, credits may be claimed in 2019, or may be deferred to 2020. Thus, acquisition placed in service may pre-date the start of credits by two or more years. This is crucially different from new construction, where the credits must be claimed no later than the year after placing in service.

Qualifying Households

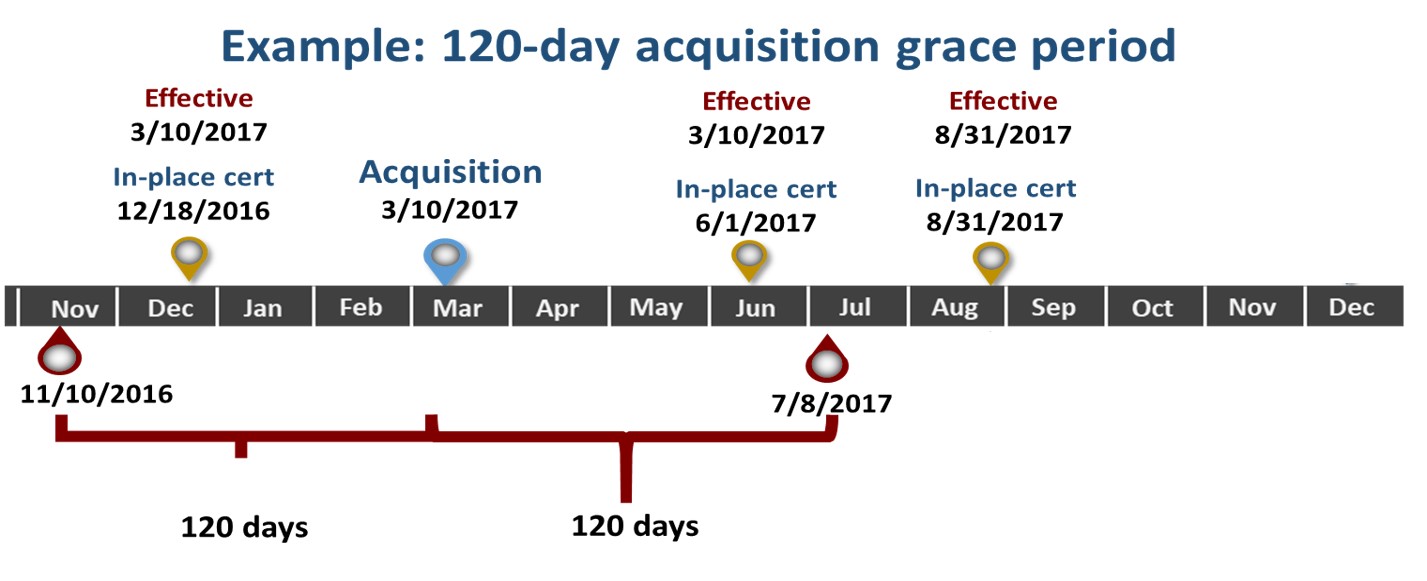

While the claiming of credits is most sensitive to the year that the rehab is placed in service, qualifying households for tax credits starts based on the acquisition date. For new construction, households are proven to qualify, and then moved in. The move-in date becomes the effective date for the tenant certification and all of the paperwork should pre-date that effective date. In many existing buildings, however, in-place households may qualify at acquisition but the IRS recognizes that it may take an owner some time to prove it after acquisition. They allow that any certification done 120 days after (or before) acquisition may have an effective date as of the acquisition placed in service. Therefore, effective dates may predate the date the paperwork is completed and signed by up to 120 days and still be compliant. Certs for households that were in place as of the acquisition date but were signed after the 120 days will have an effective date as of the date of the last household adult signature. Move-ins after acquisition will need to qualify and have an effective date as of move-in, as with any other move-ins.

In any case where credits are deferred after the year that people start occupying a building, those residents are still qualified for tax credit units once credits start, even if their income goes up over the limits by the start of the first year credits are claimed. Since acquisition may predate the start of credits by two or more years (as discussed above), the initial certs may predate the start of credits by more time than is often seen with new construction projects. However, these households are still good for the start of credits as long as IRS safe harbor provisions are followed.

As mentioned at the outset of this article, construction and dealing with the existing population provide a great deal of additional complexity than are experienced with new construction. These are beyond the scope of this article. However, understanding the above principles goes a long way in assisting compliance professionals in designing a process that can successfully deliver tax credits on an acq/rehab project amid all the other “moving parts.”

Additional Resources Available!

Our video blog series Four Things That You Must Know about acquisition/rehab projects can be viewed by clicking HERE.

Check it out HERE! The above topic is just one of many to be discussed at this year's Compliance Summit Events.

Check it out HERE! The above topic is just one of many to be discussed at this year's Compliance Summit Events.

There is a very good chance that the topic of this post is covered in an online on-demand course at Costello University.

Stay connected with news and updates!

Join our mailing list to receive the latest news and updates from our team.

Don't worry, your information will not be shared.

We hate SPAM. We will never sell your information, for any reason.